Table of Contents Show

The housing market, a once-frenzied engine of economic activity, has entered a peculiar phase. Homeowners, facing a stark contrast between their current ultra-low mortgage rates and the significantly higher rates offered today, are finding it financially advantageous to stay put. This dynamic, dubbed the “lock-in effect,” is impacting housing mobility and potentially shaping the market’s future trajectory, according to data compiled by The Kobeissi Letter on X.com, a leading source of commentary on global capital markets.

The Disincentive to Move: A Tale of Two Interest RatesThe Disincentive to Move: A Tale of Two Interest Rates

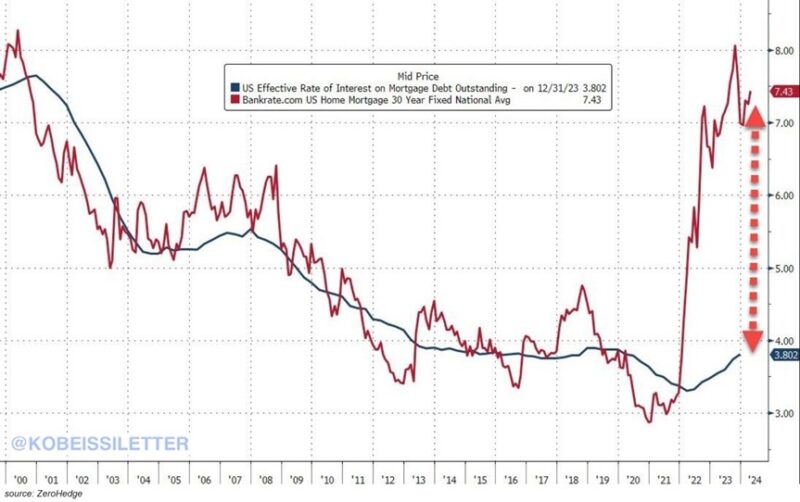

The crux of the issue lies in the yawning gap between existing mortgage rates and those offered for new loans. The effective interest rate on outstanding mortgages, a reflection of the average rate existing homeowners are paying, currently sits at a meager 3.8%. This starkly contrasts the average rate of 7.5% for new mortgages – nearly double the cost of borrowing.

For most homeowners, this disparity creates a powerful disincentive to selling. Roughly 90% of current homeowners hold mortgages below 6%, with a substantial 80% enjoying rates under 5%. A significant portion, over 20%, are fortunate enough to have secured rates under 3%. Selling their homes and taking on a new mortgage at the current, much higher rates would substantially increase their monthly payments, impacting their financial well-being.

A Market of Duality: Stagnant Inventory and Potential Price ShiftsA Market of Duality: Stagnant Inventory and Potential Price Shifts

The state of the housing market itself further amplifies this lock-in effect. The supply of existing homes for sale remains historically low. This limited inventory and the reluctance of homeowners with low rates to sell create a scenario where new home construction might take center stage.

However, the outlook for new homes presents another wrinkle. While demand for new construction might rise due to the limited options in the existing market, affordability concerns linger. With interest rates at multi-decade highs, potential buyers’ overall purchasing power weakens. Additionally, new home prices, though projected to dip below existing home prices for the first time since 2005, might not experience a significant enough decline to fully offset the impact of higher interest rates.

The Long Game: Potential Rate Cuts and Market RebalancingThe Long Game: Potential Rate Cuts and Market Rebalancing

The future trajectory of the housing market hinges on several factors, with the potential for interest rate cuts being a critical variable. If, as some economic forecasts suggest, the Federal Reserve begins to cut rates in late 2024 or 2025, the lock-in effect could loosen its grip. Homeowners hesitant to move due to the current rate environment might be incentivized to sell, injecting much-needed mobility into the market.

However, a return to historically low rates is unlikely. The era of rock-bottom interest rates that fueled the recent housing boom is likely over. A more balanced market could emerge, with interest rates settling between the current highs and the pre-pandemic lows. This would allow for a more sustainable housing activity, with existing and new homes finding buyers.

The impact of rate cuts on new home prices is also uncertain. While lower borrowing costs could increase buyer affordability, the construction industry faces headwinds. Supply chain disruptions and rising material costs could limit the extent to which new home prices decline, even with a more favorable interest rate environment.

A Market in Flux: Navigating the UncertaintiesA Market in Flux: Navigating the Uncertainties

The current housing market presents a unique set of challenges and opportunities. For homeowners locked into low rates, staying put might be the most prudent financial decision in the near term. However, for those who need or desire to move, exploring alternative solutions like bridge loans or areas with a lower cost of living could be viable options.

Prospective buyers face a different set of challenges. Higher interest rates and potentially lower affordability could make entering the market more difficult. However, the limited supply of existing homes and the potential softening of new home prices could create opportunities for those with the financial means to navigate the market.

The Bottom LineThe Bottom Line

The housing market is in a period of adjustment, with the lock-in effect as a significant force. While the future remains uncertain, the potential for interest rate cuts and a rebalancing of the market offer some cause for optimism. For homeowners and potential buyers, carefully considering financial circumstances, long-term goals, and market trends will be crucial in navigating this evolving landscape.

")